Where Will Landlords Find Most Value In The Next 5 Years?

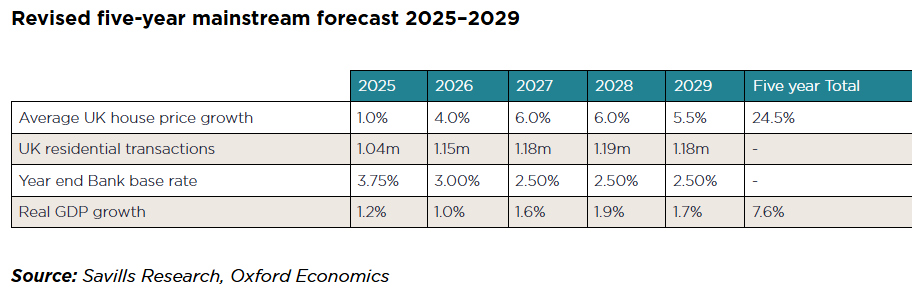

Looking ahead in the rental world can feel a bit like peering into a fogged-up bathroom mirror. You know the picture is in there somewhere, but the detail takes a moment to come through. Many landlords are asking where the real value might be for housing stock investments over the next five years? The good news is that UK residential property prices are expected to grow by 24.5 per cent over that period. However, this is only after a far gentler 1 per cent rise during 2025. It all sounds steady enough, but is there a route to greater value?

A market still catching its breath

Last year’s forecasts suggested we were heading for calmer terrain, helped along by improving sentiment and lower interest rates. Two base rate cuts have landed already this year, with more expected, and mortgage products hovering near the 4 per cent mark. It should feel like the moment the market starts lifting its head. Yet the first half of 2025 has been softer than many expected. Geopolitical upsets, tariff rows and a general sense of unpredictability have kept confidence a little fragile.

Even so, the fundamentals for medium-term growth remain intact. The shift in mortgage affordability tests is particularly important. Lenders now have more room to make decisions, including allowing more than 15 per cent of their loan book above a 4.5 LTI ratio. For landlords, that means a wider pool of potential buyers and renters whose borrowing capacity is slowly improving.

Plan Insurance can accommodate your Property Owners & Landlord Insurance needs. Just fill in our short call back form, and our professional brokers will be in contact to arrange your insurance.

Where the picture looks tricky

The top end of the housing market is expected to feel the most pressure. Concerns about possible future tax changes tend to hit the higher brackets first, and buyer jitters ahead of the Autumn Budget won’t help. Recent Nationwide data shows annual house price growth slowing to 2.1 per cent in June, compared with 4.7 per cent last December. Monthly price movements have been up and down too, with falls in three out of the first six months of the year.

Stamp Duty changes have also caused a short-term wobble in buyer behaviour. March saw the second highest sales volume for any month since 2006 as people rushed to beat the deadline. Predictably, April dropped sharply. May picked up again, but still sat around 16 per cent below normal levels for the time of year. If the usual pattern holds, we should know later in the summer whether this is just the post-deadline hangover or something more structural.

What the indicators suggest

The short-term signals are mixed. RICS reported the weakest buyer enquiries since late 2023, sitting at a net balance of minus 32 in March. Supply has remained steady, though, and sales agreed fell earlier in the year before edging back up to minus 3 in June. Normally, a gap between rising supply and softer demand suggests prices will drift down. In Q2, Nationwide recorded a 0.5 per cent fall, and stock levels remain high.

But there is a silver lining. Both Zoopla and Rightmove found that sales agreed in May were the strongest for several years, and TwentyCI data shows net sales agreed up 6 per cent year on year. The theme seems to be that while the pool of buyers is not overflowing, the ones who are active tend to be committed, needs-based movers.

Where value is likely to emerge

For landlords, the next five years are shaped by one main force: affordability. If Oxford Economics are correct, and the base rate reaches 2.5 per cent by 2027, we could see further normalisation in mortgage pricing. Combined with wage growth expected to exceed 22 per cent over the period, more renters will find themselves back in range of buying. Over time, that eases rental demand in some places but strengthens it elsewhere, particularly in areas where younger buyers still face deposit hurdles.

Relaxed mortgage stress testing creates more space for growth too. With first-time buyers’ borrowing capacity improved, landlords may find firmer resale values and a more predictable pipeline of buyers. By 2027, transactions are expected to reach roughly 1.2 million per year, close to the post the Global Financial Crisis average.

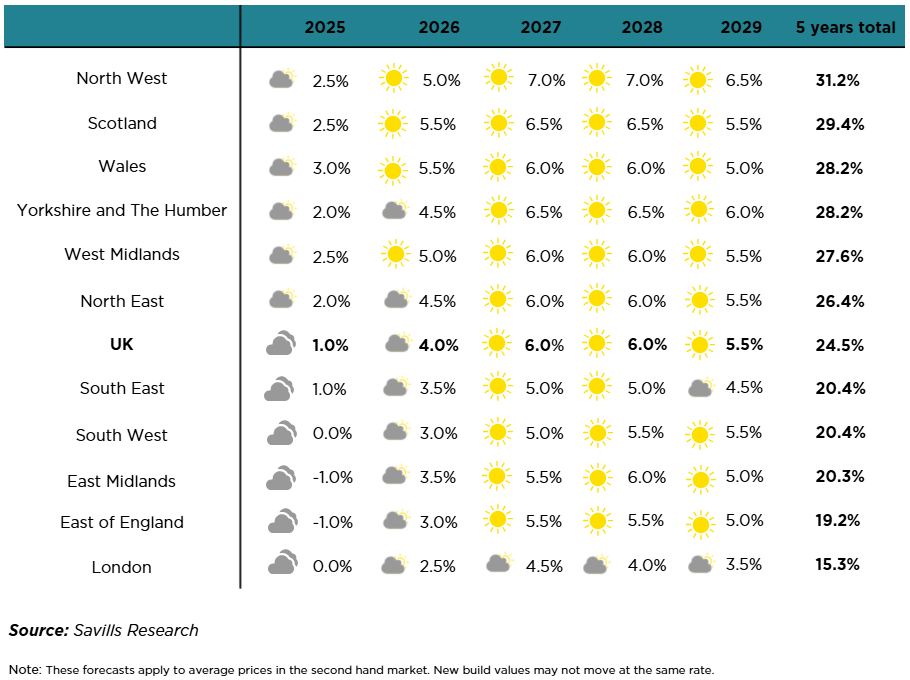

The best opportunities for house price growth appear to be in areas that are starting a lower average home value. For a landlord these areas will also need to have strong local economies to generate consistent rental demand. When combined with realistic rental pricing they may offer better long-term investment value than overheated hotspots.

Steadier growth is not as exciting as the boom years of days gone by, but for landlords that like to plan ahead, there is still plenty of promise to make their efforts worthwhile. In terms of asset appreciation the UK’s property market is forecasted to generate healthy increases, with the regions beyond the South East looking particularly rewarding according to analysis by property market experts.

The above information is not intended as investment advice. We are merely relaying forecasts and data analysis provided by companies within the property industry. Our aim to help keep our landlord clients informed with market trends. Plan Insurance Brokers can provide expert advice should you be seeking to arrange landlords and/or property insurance. To speak with a commercial insurance executive please request a call via the short form on the following page.

Find out why 96% of our customers have rated us 4 stars or higher, by reading our reviews on Feefo.