Health Insurance No Claims Discounts: How Claims Affect Premiums

What is a no claims discount, and how does it work in the UK?

If you’re a driver, you’re probably already familiar with no claims discounts (NCDs). They reward you for not making a claim on your insurance. The longer you go without claiming, often, the bigger the discount.

With car insurance, you start with no discount and build it up over time. Every year you have insurance without making a claim, the discount gets bigger – up to a maximum set by your insurer.

Many private health insurance policies also offer NCDs. They work differently, but the effect of making claims is similar – your policy will usually cost more at renewal than if you hadn’t.

How do health insurance no claims discounts work?

When you get a new private health insurance policy from a provider that offers an NCD, you’ll usually start from day one with a significant discount of up to 72% off the base premium. This is the starkest difference to motor insurance, where you start at 0% and work your way up.

This means health insurance claims can have a big impact on the policy price at renewal – particularly in the early years.

Chris Steele, founder and lead insurance expert at myTribe adds:

“Unlike car insurance no claims discounts, where there’s little to lose in the early years but plenty to gain over time, a private medical insurance no claims discount works almost in reverse, with more to lose than to gain.

The overall effect is that a no claims discount in private health insurance acts more like a penalty for claiming than a reward for not. That’s why it’s important to understand how your own no claims discount works and to compare it against what other insurers offer.”

How each UK health insurer’s no claims discount works

We’ve captured screenshots of each of the UK’s leading health insurance providers’ no claims discount scales and terms, so you can quickly browse them all. Select an insurer to view their discount, and check below the image for their key rules.

What is the NCD scale for Aviva health insurance?

Aviva’s Healthier Solutions uses a 14-level scale starting at level 12 (69% discount).

The scale runs from level 1 (0%) to level 14 (75% maximum discount).

Source: Aviva Policy Documentation 2025

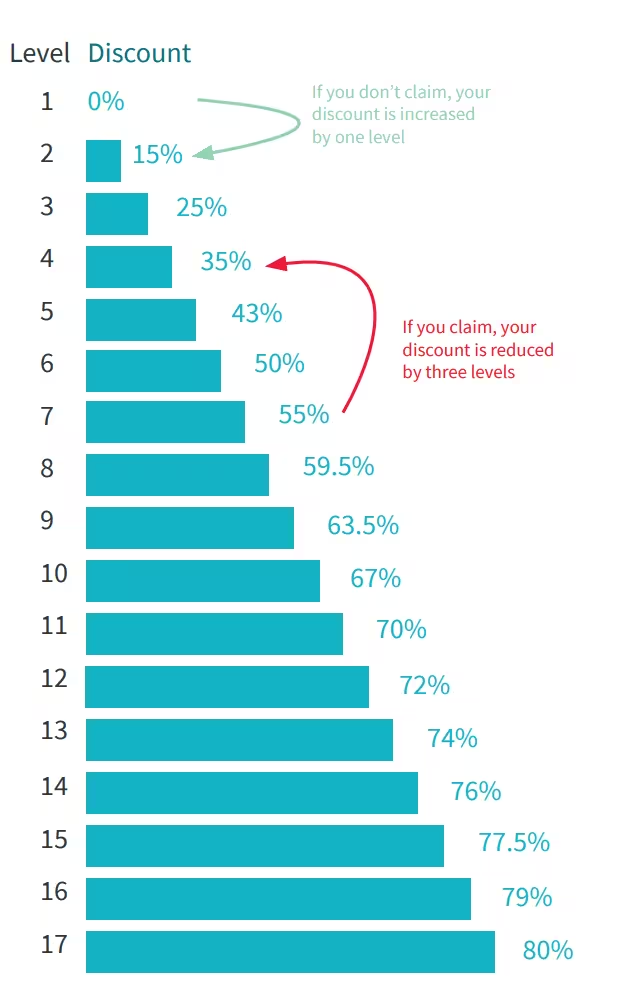

What is the NCD scale for AXA Health?

AXA Health’s Personal Health has 17 levels – the most of any major insurer.

Starting at level 12 (72% discount), you can reach level 17 for the market’s highest 80% maximum discount.

Source: AXA Health Policy Documentation 2025

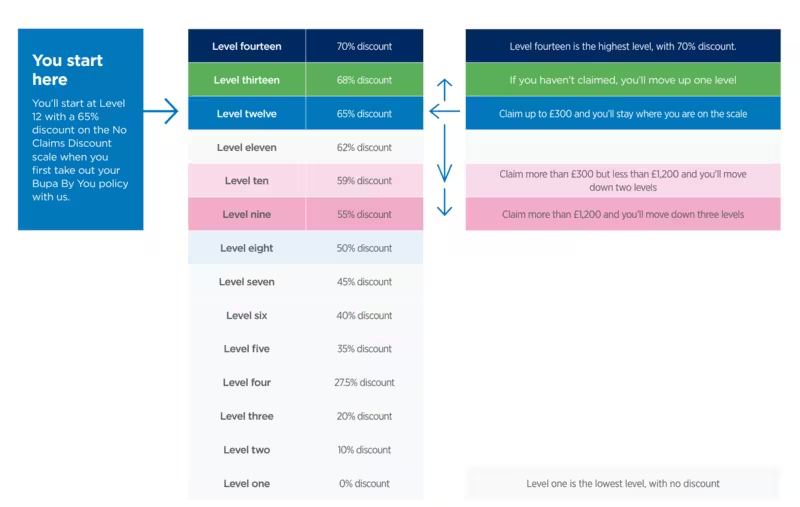

What is the NCD scale for Bupa health insurance?

Bupa By You uses a 14-level scale starting at level 12 (65% discount).

The scale runs from level 1 (0%) to level 14 (70% maximum discount).

Source: Bupa By You Policy Documentation 2025

What is the NCD scale for Saga’s health insurance?

Saga’s HealthPlan uses a 10-level scale starting at level 5 (35% discount).

The scale runs from level 0 (0%) to level 10 (60% maximum discount).

Source: Saga Health Insurance Policy Documentation 2025

What is the NCD scale for The Exeter’s health insurance?

The Exeter’s Health+ uses a 15-level scale starting at level 12 (70% discount).

The scale runs from level 0 (0%) to level 15 (75% maximum discount).

Source: The Exeter Policy Documentation 2025

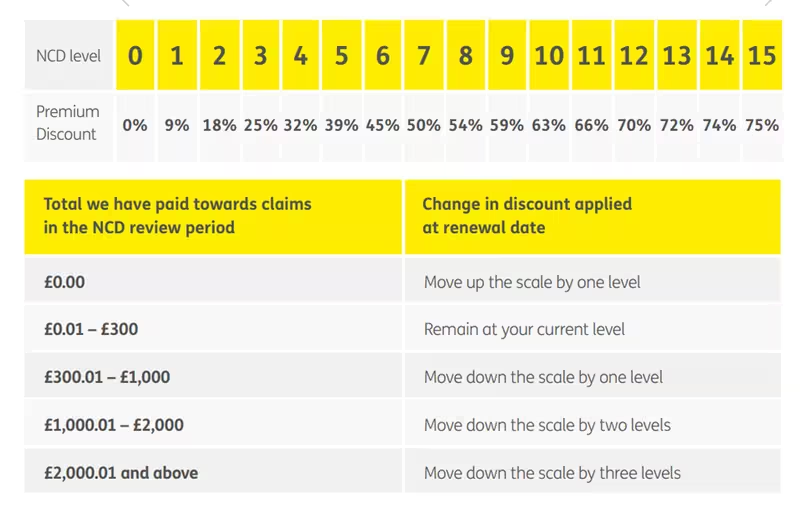

What is the NCD scale for WPA’s health insurance?

WPA’s Complete Health uses a 14-level scale starting at level 12 (64% discount).

The scale runs from level 0 (0%) to level 14 (70% maximum discount).

Source: WPA Policy Documentation 2025

Click anywhere or press ESC to close

Pretty confusing, right?

As you can see, there’s significant variation across insurers – different levels, starting points, percentages and rules. Let’s break this down to make it easier to compare.

Comparison of health insurer NCD starting levels

Most private medical insurance plans start around the top of its no claims discount scale, often around level 12 of a possible 14-17 levels.

- No claims in a policy year: You typically move up one level, increasing your discount slightly.

- Making a claim: You may drop multiple levels in one year, depending on the claim size and insurer’s rules.

As you can see from the table, Saga is an exception, as it starts most new policies midway through its discount scale at level five. Although both the starting and maximum discounts are lower than other providers, it doesn’t mean that Saga’s NCD is better. It penalises claims more heavily and the NCD is per policy, not person – more on that later.

Will your medical insurance get cheaper if you don’t make a claim?

No, it’s very unlikely your health insurance renewal quote will be lower, even if you don’t make a claim. There are many things that affect the cost of a health insurance policy. For example, age. As we get older, we’re more likely to suffer from health problems and more likely to make a claim on our insurance.

Providers will factor this into their pricing – along with other factors, including medical inflation – when they give you a renewal quote. The cost of your insurance won’t necessarily go down if you don’t make a claim, but it will be cheaper than if you had.

Claim impact on health insurance discounts

It’s not very simple to compare UK health insurance providers’ NCDs because they use different scales. Some have more levels than others, and the percentage discounts associated with each level aren’t always the same.

Something all of those that offer an NCD have in common though is that the amount of discount offered between levels gets larger the further down the scale you fall. In other words, you lose a larger percentage of your NCD the more you claim.

How claims of different sizes affect your NCD

Although it’s not easy to compare providers directly, one difference between them is how NCDs are affected by smaller claims.

Expert insight

As you can see from the table, some private health insurance providers are more lenient when it comes to smaller claims.

The Exeter, for example, won’t change your no claims discount level until claims reach £300, and you won’t move down three levels until they reach £2,000. AXA Health’s Personal Health policy, on the other hand, will move you down three levels for claims of any size.

This isn’t an exact comparison, because the percentage discounts associated with the levels differ. And even the percentages aren’t as important as the pounds and pence figures behind them. But it’s still useful as a guide for how providers treat smaller claims differently.

Saga does things quite differently from the rest

One major provider we haven’t included in the above table is Saga. This is because it doesn’t assess claims based on the total cost in a policy year. Instead, Saga will move you down two levels for every claim you make. So if you make multiple claims in a single policy year, you could lose your NCD much more quickly.

Another key difference with Saga is that its NCD is per policy, not per person as it is with the other providers mentioned in this article. This means all claims have the same impact on the NCD, no matter who makes them.

How Saga’s policy wide NCD compares to other insurers’ per person approach

If you consider a family policy with two adults in their 50s and two teenage children, we’d expect 80-90% of the cost of the policy to be due to the adults on the plan.

With any of the insurers we’ve covered in this article, bar Saga, each family member would have an NCD, so if a child claimed and their discount was affected, or even fully lost, it likely wouldn’t have a huge impact on the overall cost.

By contrast, Saga’s approach of a shared NCD would result in a very different outcome, as the child’s claims would affect the “shared” discount, likely resulting in a significant price rise.

Do all health insurance providers offer a no claims discount?

Most private health insurance providers in the UK offer NCDs in some form, but not all of them use a sliding scale. Vitality, for example, uses its own “ABC” model:

So despite not using a sliding scale, claims are still an important factor that will affect the cost of your policy at renewal.

Some, like Freedom Health Insurance, claim to not offer an NCD at all. Although it’s likely that your claims history will still be a factor in your renewal price.

Types of claims that won’t affect your no claims discount

Some claims won’t affect your NCD at all. This varies between providers, but generally the following types of claims won’t see you move down any levels on the NCD scale:

- Cash benefits – e.g. dental, optical and NHS

- Remote GP consultations

- Helplines and support services

Another thing to note is that any claims you make below your excess amount won’t affect your NCD. This is because your insurer won’t need to pay out unless your claim exceeds your excess.

Your excess and how it affects your no claims discount

Your excess is the amount you have to contribute towards a claim. For example, if you choose a £500 excess and the cost of your treatment is £2,000, you’ll pay £500 and your insurer will pay the rest.

Most insurers let you choose your own excess, and it’s directly related to the cost of your policy. If you choose a higher excess, you will pay a lower price for your cover.

This is important because any claim you make under the excess amount won’t affect your NCD. Setting a higher excess may make you shoulder more of the initial cost, but it could save you money in the long run. The right choice for you will be an individual one, but it’s worth considering when choosing the excess for your policy.

Protecting your no claims discount

Some insurers will give you the option of protecting your NCD. This means you’ll pay a bit more for your insurance, but won’t lose your discount if you make a claim. Not all providers offer this, but some (e.g. Aviva, AXA Health) do.

If you claim on your health insurance while your NCD is protected, you’ll lose the protection for a period – usually one or two years. If you don’t make another claim in that time, you’ll be able to add NCD protection again.

What you need to consider about private health insurance no claims discounts

Most health insurance providers offer NCDs in one form or another, but they don’t work in the same way as motor insurance NCDs. Many of them use sliding scales, which means you have more to lose than gain.

Variations in how these scales work make comparing providers difficult. The differences largely come from how much you can claim before you move down the scale and how far down you move.

Providers that allow small claims without affecting your NCD may offer more protection. But if you claim consistently and for large amounts, you’ll end up at the bottom of the scale, no matter who your insurer is.

Levels and percentages aren’t as important as the pounds and pence figures behind them. The higher the base premium, the more it will be affected by dropping down levels on the NCD scale.

Your excess can have a big impact on your NCD. A higher excess may make treatment more expensive, but it could save you money in the long run. It will also reduce your premium. In some cases, it may even save you money to pay for treatment yourself.

Disclaimer: This information is general and what is best for you will depend on your personal circumstances. Please speak with a financial adviser or do your own research before making a decision.